The Ecommerce Dilemma

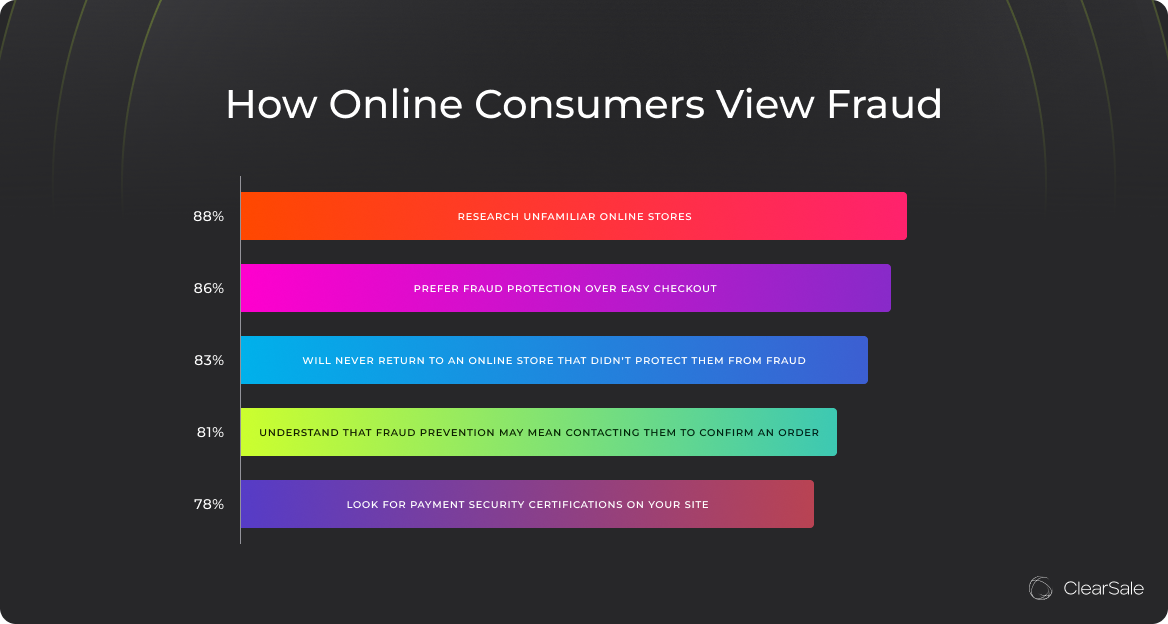

In today’s ecommerce market, companies have to place a heavy focus on customer experience (CX) to attract and maintain a loyal customer base. Among the many factors that impact CX is fraud prevention. Our original research revealed that 83% of customers won’t return to a retailer that failed to protect the customer from fraud.

That presents online businesses with a dilemma. They need to bring their fraud prevention “A” game to provide a superior customer experience without making it a hassle. Easy, right? Not so much. Especially when companies have to combat more fraud than ever.

Fraud teams are busier than ever

Fraudsters have taken advantage of the recent ecommerce explosion with new tactics and schemes. From scams to fake charity websites to criminals pretending to offer IRS stimulus checks, the Federal Trade Commission received nearly 5 million fraud reports from consumers in 2020 and 2021, equaling US$3.5 billion in losses.

And a Juniper Research study titled “Online Payment Fraud: Market Forecasts, Emerging Threats & Segment Analysis 2023-2028” estimates that ecommerce payment fraud will exceed $362 billion cumulatively through 2028.

To fight fraud effectively, companies need to know trends and recognize patterns. Here are some of the most prevalent fraud trends to recognize.

ATO fraud

A type of identity theft, account takeover (ATO) fraud occurs when a fraudster uses a piece of a victim’s identity, like their Social Security number or email address, to access and take over the victim’s account. ATO fraud accounted for every fifth login attempt and 13% of U.S. ecommerce fraud costs in 2021.

How does ATO fraud happen? Criminals use several tactics to get customer information:

Phishing: These scams happen when a fraudster sends a link via email, text message or even social media using well-established website interfaces that seem trustworthy. When the user clicks on the link, it automatically installs software that gives the fraudster access to the user’s device.

Malware: When fraudsters install malicious software on a victim's computer, it lets the fraudster capture keystrokes as the user enters login IDs, passwords and emails. Using that data, fraudsters access the victim's accounts and make fraudulent purchases.

.jpg)

Triangulation fraud

Triangulation fraud happens when an innocent customer makes a purchase on a third-party marketplace, except the item they receive was fraudulently purchased from another retailer’s website.

Friendly fraud

Friendly fraud happens when a customer pays with a valid card but then claims their order never arrived, that it was damaged or that it was substantially different from the product description on the website.

Policy abuse

Policy abuse encompasses a wide variety of schemes that fraudsters attempt in an effort to take advantage of online companies and their business policies. This can show up in multiple ways:

Loyalty fraud: Loyalty fraud happens when a fraudster hacks into a consumer’s personal information and takes over their loyalty points to redeem benefits.

Coupon abuse: Coupon or discount abuse happens when a fraudster creates multiple accounts so they can use a promotion more than once.

Gift card fraud: Gift card fraud happens when fraudsters access the activation codes on gift cards and use them to make purchases with little to no tracking.

Return abuse: Return abuse describes fraud types that involve criminals taking advantage of an ecommerce company’s return policy. This includes stolen merchandise returns, receipt fraud, insider fraud, bricking and wardrobing.

Fraud-as-a-service (FAAS)

One of the more recent fraud trends, fraud-as-a-service (FAAS) involves renting bot networks from fraud "service providers" to launch large-scale fraud campaigns against websites. This type of fraud can easily overwhelm a business because they don’t necessarily recognize the problem until it’s too late.

How should companies address all these fraud types? Often, ecommerce businesses resort to a number of tactics — many with unintended consequences.

Businesses rely heavily on fraud filters

Just about every ecommerce platform comes standard with fraud filters that use transaction screening and algorithms to fight fraud, including:

AVS (billing and shipping address) matching

Card verification number (CVV)

Transaction amount

IP addresses

Geolocation

Email confirmation

Device fingerprinting

External data sources

While fraud filters are useful, they tend to be overly strict. So, when they’re a company’s only line of defense, fraud filters often end up automatically declining valid orders without the company even knowing they’ve lost business.

Understanding False Declines

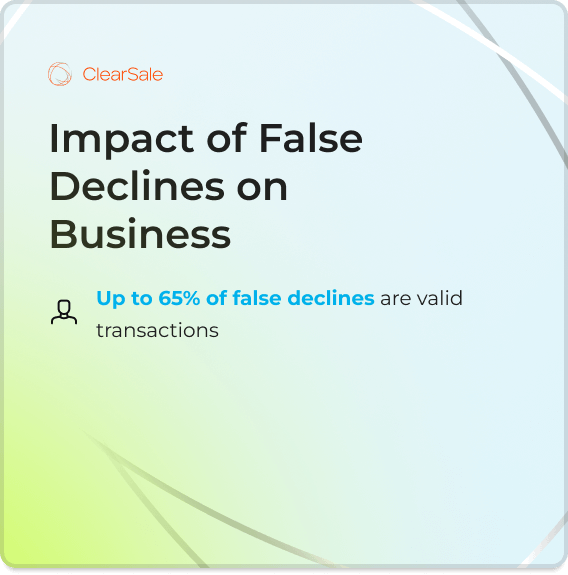

False declines — sometimes called “false positives” — happen when a customer’s valid order is declined because the business mistakes it as fraudulent.

A false decline doesn’t necessarily mean that the transaction won’t eventually go through. There are two types of declines:

Hard declines are the result of an error or issue that cannot be resolved immediately. The decline isn’t temporary, and subsequent attempts with the same payment method will likely not be successful. Customers often walk away from false declines angry and embarrassed.

Soft declines are due to temporary issues and can be retried. Subsequent transaction attempts with the provided payment method information may process successfully. This is dependent on the customer’s willingness to retry the purchase.

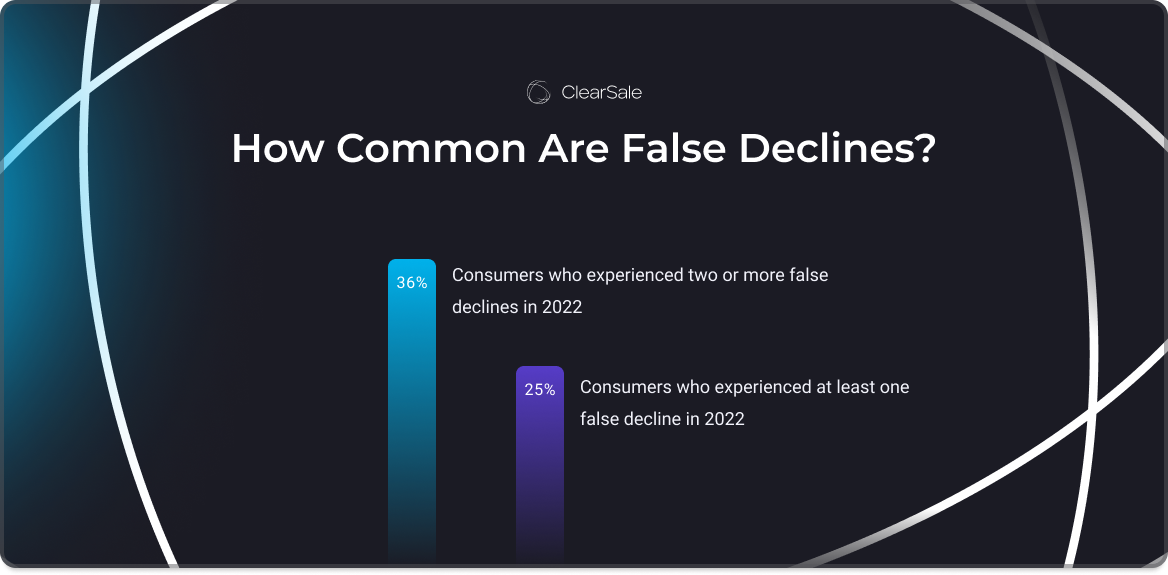

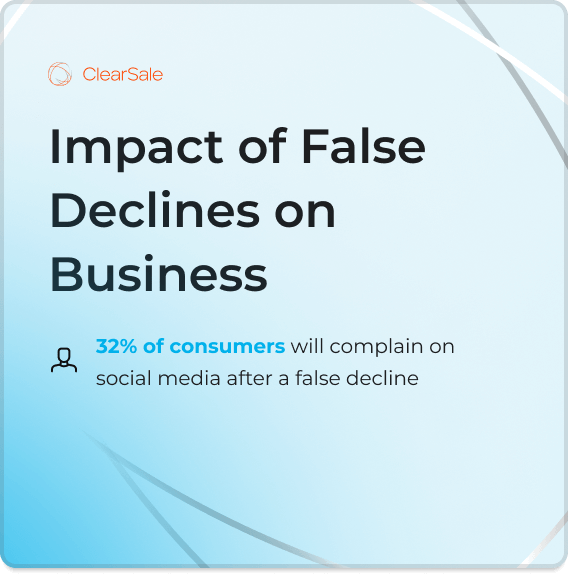

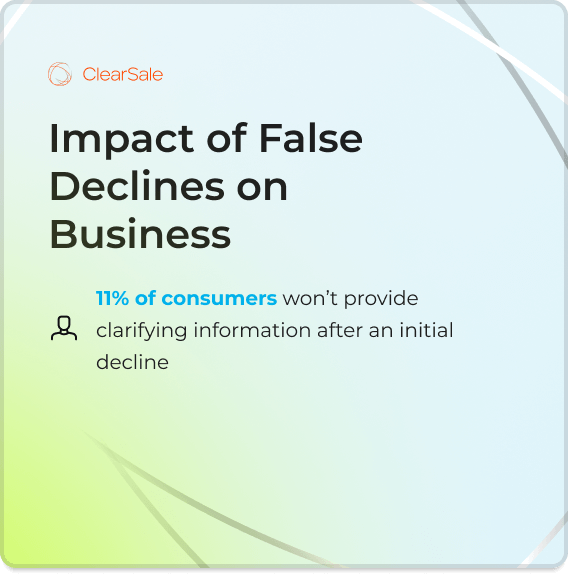

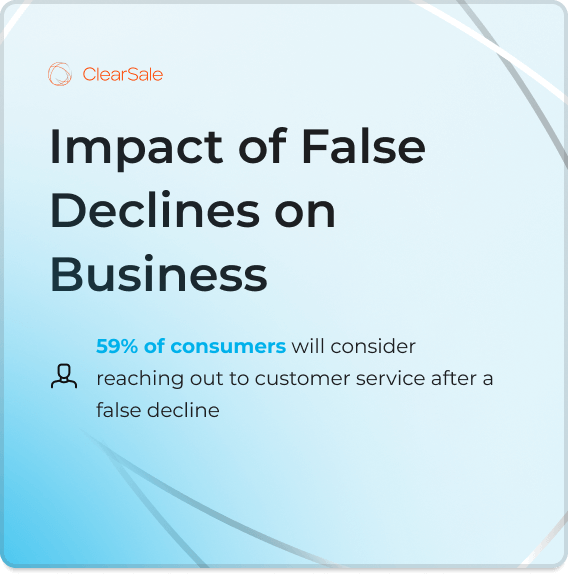

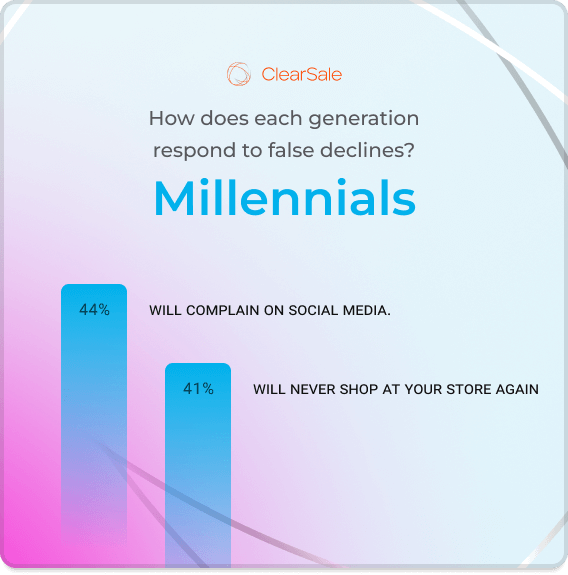

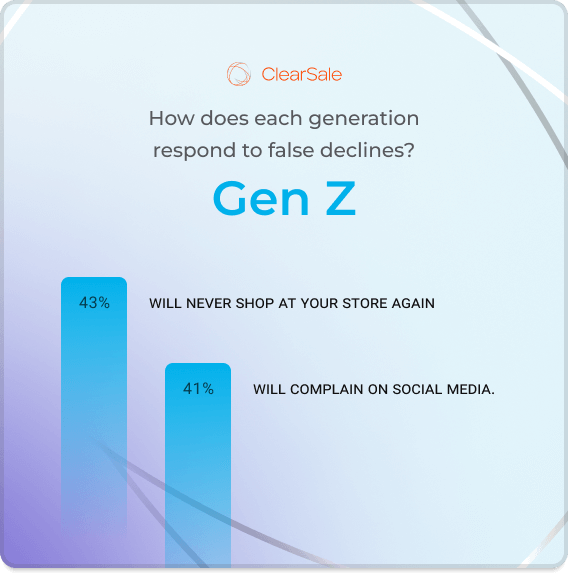

Unfortunately, false declines are quite common. Our original research shows that 25% of respondents experienced at least one false decline in 2022, and 36% of those customers experienced two or more false declines. Even when customers experience a soft decline, where they could try the transaction again, our research revealed that only 22% of customers definitely would do it. This can create issues for businesses as well.

.png?width=925&height=300&name=rounded-in-photoretrica%20(1).png)

.png?width=448&height=493&name=rounded-in-photoretrica%20(2).png)